In what amounts to yet another indication of souring market sentiment, on Friday, February 4, Brazil-based payments unicorn EBANX yanked its IPO plans, initially scheduled for Q1 of 2022. The Brazilian payments darling first filed for its U.S. IPO back in October of 2021. This following the completion of one of the largest funding rounds ever by a Brazilian fintech, with a $430M USD investment from global private equity firm Advent International in June. The funding allocation provided $400M for growth, and $30M for the anticipated 2022 IPO. EBANX wasted no time putting those monies to good use, as in rather short order, it went on to acquire Brazilian money transmitter Remessa Online for $229M USD in December.

Though the pace and magnitude of EBANX’ late 2021 growth initiatives were frenetic and extraordinary respectively – EBANX also acquired voucher payment and billing platform BoletoBancario.com, and finalized its acquisition of Juno, both in Q4 – they were roughly commensurate with its organic performance, which in terms of growth, was exponential. The company stated that year-end total processing volume for 2021 came in at double what it pushed through in 2020 (reportedly $3.5B).

Drivers of growth…

It can be argued that EBANX has carved out a fertile niche for itself in the LATAM payments landscape. It markets itself as a plug-and-play, two-sided payments platform for LATAM merchants and consumers, crisscrossing the region with a functional footprint spanning 15 countries, and offering 100 different methods of payment. But EBANX’ key value proposition, and perhaps what it’s best known for – and why it has attracted so much attention from investors – is its platform’s ability to facilitate client billings on behalf of some the world’s largest multi-national companies, such as Spotify, Uber, and Amazon. These global heavyweights use EBANX for cross-border authorization and settlement, FX, smart routing, and, in the case of Uber, pushing Gig-economy, 1099 worker payouts into virtual wallets, settling in worker’s native currency.

EBANX’ improving technology is also contributing to growth, leveraging a new hybrid platform – EBANX ONE – for better accommodating the same class of large corporate partners. The new technology increases the platform’s throughput to 300 transactions per second with less than one second latency.

All in, EBANX is connecting 70 million Latin Americans to global products and services through its payment platform, and that’s roughly 10% of its TAM of 660 million.

Economically, EBANX’ success can be directly attributed to having created a two-sided technology platform conducive to massive network effects. The platform’s primary value proposition lies in its ability to connect LATAM’s massive underbanked population with the world’s largest content providers, online marketplaces, and gig-economy firms.

EBANX has an extremely compelling growth story, one that makes prioritizing access to U.S. capital markets the logical next step in its evolution.

And yet the IPO got yanked.

Investment banking take…

EBANX is an attractive asset. It has an excellent management team, strategy, and strong financial backers – Boston-based Advent International’s pedigree in international financial technology, payments, and software is top-notch.

Its raison d’être – enabling a massive TAM of LATAM consumers, many of them underbanked and without access to basic financial services, to efficiently transact with global purveyors of high-demand products and services – continues to justify itself by virtue of its own performance.

Along with recently-gone-public Brazilian fintech NuBank, which I wrote about a few weeks back, I think EBANX is one of LATAM’s higher quality fintech assets. So, when EBANX eventually does go public, and it will, the stock should do well provided its investment bankers price it correctly.

Software & Fintech Investment Banking – NuBank

Software & Fintech Investment Banking – NuBank I still maintain that NuBank’s last minute downward revision of its IPO price was a rare instance (unfortunately these days) of investment bankers doing the right thing for the company and shareholders, versus themselves. Similarly, and admirably, I think EBANX and its investment bankers are also doing the right thing by yanking its Q1 IPO.

The equity markets are simply too volatile right now. Especially for technology companies whose price movement, when compared to slower-growth, value stocks, moves disproportionately to interest rate fluctuations. As this is the macro-backdrop against which tech equities must navigate at the moment, the volatility will likely continue to be a challenge to new issues, until such time as inflation stabilizes.

But further to avoiding the current environment of heightened volatility, it was right for EBANX and its investment bankers to yank its IPO because at the same time, we’re also experiencing sector contagion in fintech and payments stocks.

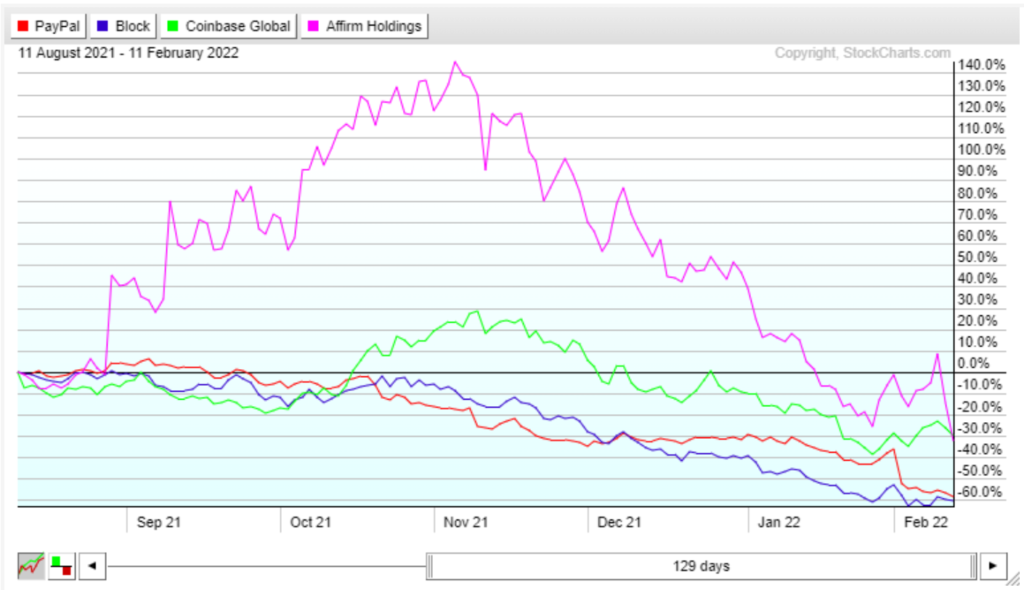

The last six months have not been kind to many of fintech and payment’s big-names, especially those which were the beneficiaries of changing consumer preferences caused by the pandemic. Four of the most noteworthy being PayPal, Block, Coinbase and Affirm.

Software & Fintech Investment Banking – 6 Month – PYPL, SQ, COIN, AFRM

Software & Fintech Investment Banking – 6 Month – PYPL, SQ, COIN, AFRM

Layering on sector contagion to heightened volatility and declining sentiment, it was the right decision to pull EBANX’ IPO. Otherwise, EBANX, its investors and shareholders would have had to rely on market timing for a successful launch – and that, almost never, produces optimal outcomes.