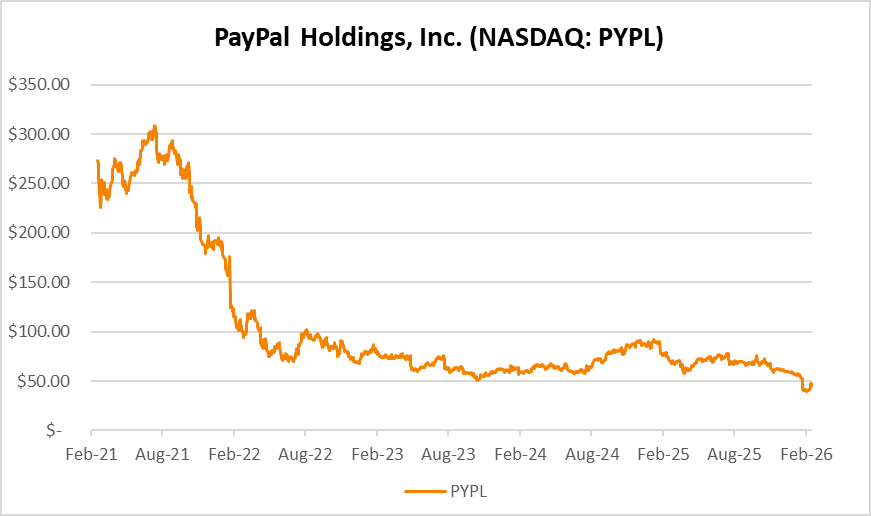

Recent speculation about a potential acquisition of PayPal (NASDAQ: PYPL) has intensified, driven by its significant stock decline. The shares have fallen 40% over the past year, from a high of around $78 in July 2025 to the current level of approximately $46. This sharp drop has been fueled by intensifying competition in the digital payments space, slow growth, uneven consumer spending, and recent management changes, including the CEO. Reports indicate numerous unsolicited interests from potential buyers, with discussions involving investment banks and suitors evaluating either the entire company or specific assets, such as the consumer-focused Venmo app or the merchant processing platform Braintree.

Let us explain.

Stripe, the well known privately held B2B payment infrastructure leader with a recent valuation of $159 billion, has emerged as a prominently mentioned name and could reshape the US payments ecosystem. Bloomberg and other sources reported that Stripe has expressed preliminary interest in acquiring all or parts of PayPal. However, subsequent reports indicate that PayPal is not actively seeking a sale, is not engaged in formal talks with Stripe, and has been collaborating with advisors to prepare defenses against possible hostile takeovers or activist investor campaigns. Nonetheless, the persistent and widespread media coverage has kept the acquisition narrative alive. We reiterate no deal is confirmed.

We recognize there are numerous potential suitors seeking PayPal’s assets but a deep industry dive into all the possible combinations is not practical in this forum. Consequently, today, we are focusing on why Stripe may make sense as a natural acquirer.

Access to Massive Consumer Base and Data

PayPal boasts over four hundred million active consumer accounts, many linked directly to bank accounts, providing a rich “consumer graph” of data and funding sources. Conversely, Stripe, which excels in B2B and merchant-side infrastructure, lacks a strong consumer-facing brand or direct access to such a scale of end-user data. Acquiring PayPal would allow Stripe to integrate consumer identities into its ecosystem, enhancing services like fraud detection, underwriting, and personalized financial offerings. In the US, this could accelerate Stripe’s push into consumer payments, where PayPal’s wallet and Venmo dominate P2P transfers, giving Stripe raw material to build AI-driven tools or stablecoin integrations without starting from scratch.

Complementary Assets for a Two-Sided Platform

Stripe is merchant-focused, but PayPal offers key consumer-side components: its digital wallet, branded checkout, Braintree (a competing merchant processor), and Venmo. Merging these would transform Stripe from an infrastructure provider into a full-platform player with control over the entire commerce flow, including pricing, payment routing, and method presentation at checkout. This vertical integration addresses the payments industry’s “structural inversion,” where infrastructure (Stripe’s strength) triumphs over standalone consumer brands (PayPal’s model), which are increasingly commoditized. In the US, it would reduce Stripe’s reliance on third-party wallets and partners like Shopify (over 50% of Stripe’s revenue), while neutralizing competition from PayPal’s assets.

Competitive Edge Against Tech Giants

The US payments space is evolving with rivals like Apple Pay and Google Pay disrupting traditional models. For instance, Stripe could bypass card rails (e.g., Visa/Mastercard) for direct account-to-account payments, cutting interchange costs and improving margins. Combined, the entities would process over $3.6 trillion annually, creating the largest non-card-network payment system and boosting Stripe’s leverage in negotiations with banks and merchants.

A full acquisition would be massive (few entities can easily “swallow” a ~$40B company), and regulatory hurdles could complicate big tech involvement. Private equity or a breakup/sale of parts (e.g., consumer wallet vs. merchant processing) might be more feasible. Yet the slumping stock price may make PayPal an attractive “value” target amid fintech consolidation trends. We are keeping an eye on updates, as new CEO leadership and activist pressure may influence outcomes.

Other potential buyers discussed in analyst commentary and reports include:

- Big Tech companies such as Apple (frequently mentioned for its Apple Pay dominance and potential to bolster digital wallet capabilities), Alphabet (Google), Meta, Amazon, and Microsoft. These could face regulatory scrutiny but have the scale and strategic interest in payments ecosystems.

- Private equity firms are a possibility for a full acquisition, given PayPal’s strong balance sheet and cash flow, allowing a leveraged buyout at a premium without immediate antitrust issues.

- Other payments and fintech players mentioned include Adyen, Block (Square), or even legacy networks like Visa/Mastercard (though less likely for a full deal due to size/overlap). For specific assets, names like JPMorgan Chase, American Express, or Revolut have been floated (e.g., for Venmo).

- Wildcard mentions include Elon Musk (PayPal co-founder with “everything app” ambitions via X), though liquidity constraints make this improbable. Some outliers like Walmart have also been mentioned.