Nacha, now rebranded in lowercase rather than all capital letters, stands for the National Automated Clearing House Association. As a nonprofit organization, Nacha manages and governs the ACH Network, the primary system for electronic funds transfers in the United States, including direct deposits, bill payments, payroll, and Same Day ACH transactions. Nacha recently increased its per payment ACH transaction limit to $10 million from $1 million. This is an important development for the high-volume ACH network.

Let us explain.

Nacha sets the rules that ensure the ACH system operates reliably for all participating banks and credit unions. At its recent Smarter Faster Payments Conference, Nacha announced an increase in the Same Day ACH per-payment limit, effective September next year. This marks the third major expansion for the service, which originally launched with a $25,000 limit, was raised to $100,000 in 2020, and then to $1 million in March 2022. The new $10 million ceiling aligns Same Day ACH with other faster payment systems, such as The Clearing House RTP and FedNow, both of which increased their limits to $10 million in 2025. The primary goal is to support higher-value, time-sensitive payments for invoice and tax payments, insurance claims, payroll funding, merchant settlements, and cash concentration. By removing the previous $1 million cap, Same Day ACH becomes significantly more competitive for B2B and corporate treasury applications.

Can you tell us more about ACH? We are glad you asked.

On June 22, 2024, we wrote “The Automated Clearing House (ACH) is a payment processing network electronically enabling bank account-to-bank account transactions by connecting all 12 Federal Reserve banks to the 5,000 or so member financial institutions in the US.

Businesses utilize ACH for a wide variety of payments to their employees, such as payroll and T&E reimbursement, and smaller dollar value business-to-business bill payments. Consumers may not realize it but they also use ACH when a credit or debit card is presented for payment; the back-end settlement is an ACH business-to-business payment from the card issuing institution to that retailer’s bank. Furthermore, any time a consumer writes a check to another individual or a business, that instrument is settled between the two parties’ bank accounts over the ACH network. Originally designed to electronically deliver government benefits, like Social Security in the 1970s, today it moves $15 trillion by direct deposit into consumer bank accounts for payroll and other services on an annual basis. Consumer bill payments constitute about $10 trillion. So, when combined with direct deposits the total is commensurate with the U.S.’ GDP annually, or approximately $25 trillion dollars.

The biggest change to ACH over the years has been speed – what once required three or more days to clear is now one or two. What’s more, same day ACH is now available for certain fees. Non-member Federal Reserve banks may utilize ACH if they meet certain criteria or participate on a similarly functioning but different network for real-time-payments called The Clearing House.”

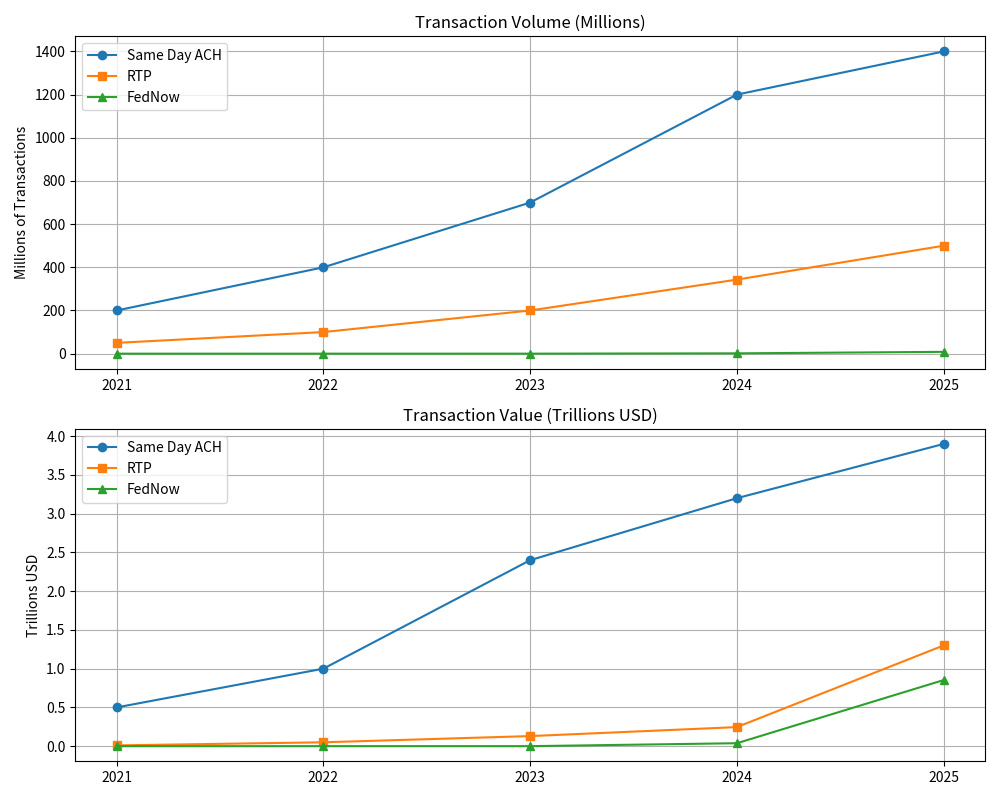

What is the difference between ACH, The Clearing House RTP and FedNow Services?

Same Day ACH, governed by Nacha, is a batch-processed service that allows same-business-day settlement through three daily processing windows on weekdays. It offers broad universal participation across all U.S. banks and credit unions, making it accessible and cost-effective for higher-volume, planned payments multiple days in advance. However, it is not truly instant and is limited to business-day windows.

The Clearing House RTP Network, a private real-time payment system launched in 2017, and FedNow Service, the Federal Reserve’s public real-time system launched in 2023, both provide true instant payments that settle in seconds with irrevocable finality, 24/7/365 availability (including weekends and holidays), and immediate access to funds for recipients. RTP, operated by a bank-owned consortium, has strong adoption among larger institutions and excels in high-value B2B, treasury, and corporate payments, with added features like messaging and request-for-payment.

FedNow, as a public utility, emphasizes broad accessibility for institutions of all sizes and focuses on safety, resiliency, and inclusion. In summary, Same Day ACH is effective for cost-efficient, high-volume same-day (but not instant) payments with universal reach. On the other hand, RTP or FedNow, when true 24/7 immediacy and finality are required, with RTP often preferred for complex corporate needs and FedNow for widespread public infrastructure. Many organizations use all three in combination depending on urgency, cost, and recipient coverage.

Conclusion

Consumers and businesses around the world have increasingly turned to stablecoins such as USDT and USDC for fast, low-cost, same-day domestic and cross-border transactions. While the United States currently lags many of its international counterparts in this space, the gap can be narrowed by expanding competitive payment alternatives within the U.S. ecosystem, including enhancements like the upcoming increase in Same Day ACH limits. Furthermore, once passed and clarified, the Genius Act and Clarity Act could function as powerful catalysts, delivering the regulatory support needed to accelerate innovation and growth in digital payments. More to follow.

Source: The Federal Reserve and The Clearing House